Website Last updated:

July 3, 2026

Taxation of Family Foundations

Corporate Tax Guide | CTGFF1

May 2025

Contents

1. Glossary

2. Introduction

2.1. Overview

2.2. Purpose of this guide

2.3. Who should read this guide?

2.4. How to use this guide

2.5. Legislative references

2.6. Status of this guide

3. What is a Family Foundation?

3.1. Overview

3.2. Foundations

3.3. Trusts

3.3.1. Unincorporated trusts

3.3.2. Incorporated trusts

3.4. Similar entities

3.5. Entities wholly owned and controlled by a Family Foundation

4. Overview of Corporate Tax

4.1. Persons subject to Corporate Tax

4.2. Exempt Persons

4.3. Certain income of natural persons not subject to Corporate Tax

4.4. Family Foundations under the Corporate Tax Law

5. Conditions to be a Family Foundation

5.1. Beneficiary condition

5.2. Principal activity condition

5.3. No Business Activity condition

5.4. No tax avoidance condition

5.5. Distribution condition where beneficiaries include public benefit entities

5.6. Foreign entities and Family Foundations

6. Multi-tier structures

7. Corporate Tax implications for a Family Foundation that is treated as an Unincorporated Partnership

7.1. Family Foundation

7.2. Natural person beneficiary

7.3. Public benefit entity beneficiary

7.3.1. Income attributable to a public benefit entity

7.4. Deductible expenditure

7.5. Payment to beneficiaries for services provided to a Family Foundation

7.6. Foreign Tax Credit

7.7. Distribution by a Family Foundation to its beneficiaries

8. Tax compliance

8.1. Registration for Corporate Tax purposes

8.2. Application to be treated as an Unincorporated Partnership

8.2.1. Foreign entities

8.2.2. Multi-tier structures

8.3. Annual Confirmation of the Family Foundation

8.3.1. Annual Confirmation by a Family Foundation

8.3.2. Annual Confirmation by an Unincorporated Partnership

8.4. Failure to continue meeting the conditions

9. Updates and Amendments

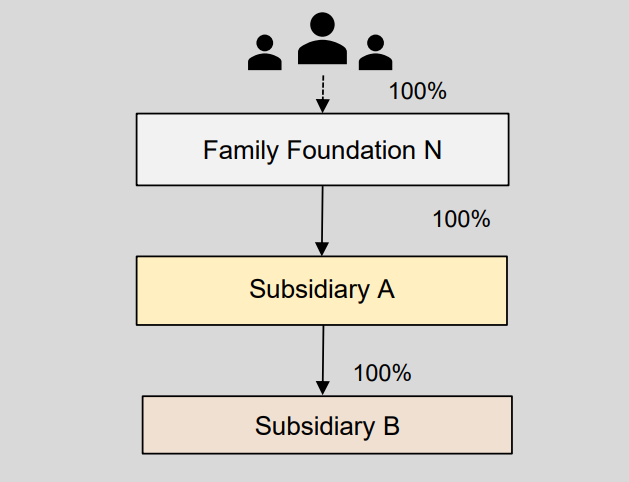

Corporate Tax treatment for Family Foundation N:Corporate Tax treatment for Subsidiary A:Corporate Tax treatment for Subsidiary B:

Corporate Tax treatment for Family Foundation N:Corporate Tax treatment for Subsidiary A:Corporate Tax treatment for Subsidiary B:Corporate Tax treatment for the family members who are beneficiaries

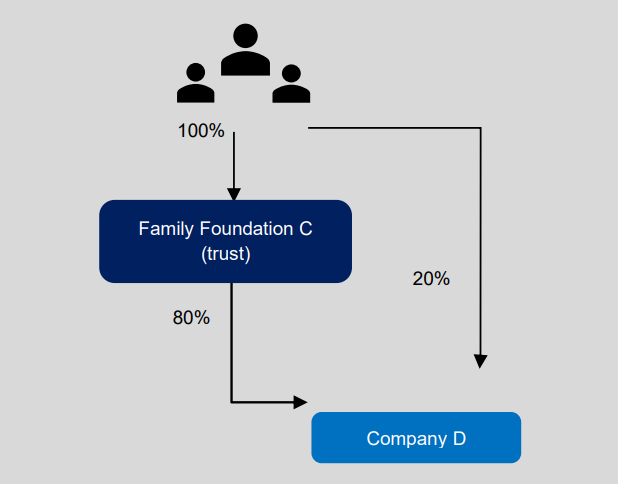

Corporate Tax treatment for Family Foundation C

Corporate Tax treatment for Family Foundation CCorporate Tax treatment for Company DCorporate Tax treatment for the family members who are beneficiaries

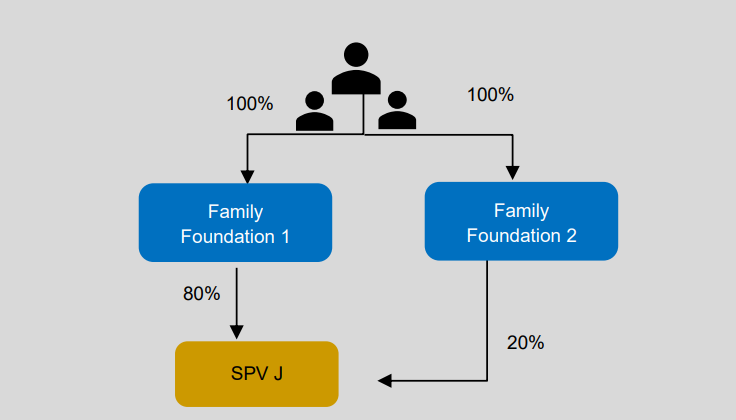

Corporate Tax treatment for SPV JCorporate Tax treatment of the family members who are beneficiaries

Corporate Tax treatment for SPV JCorporate Tax treatment of the family members who are beneficiaries Distribution condition for Foundation SCorporate Tax treatment for Ms P and Mr Q

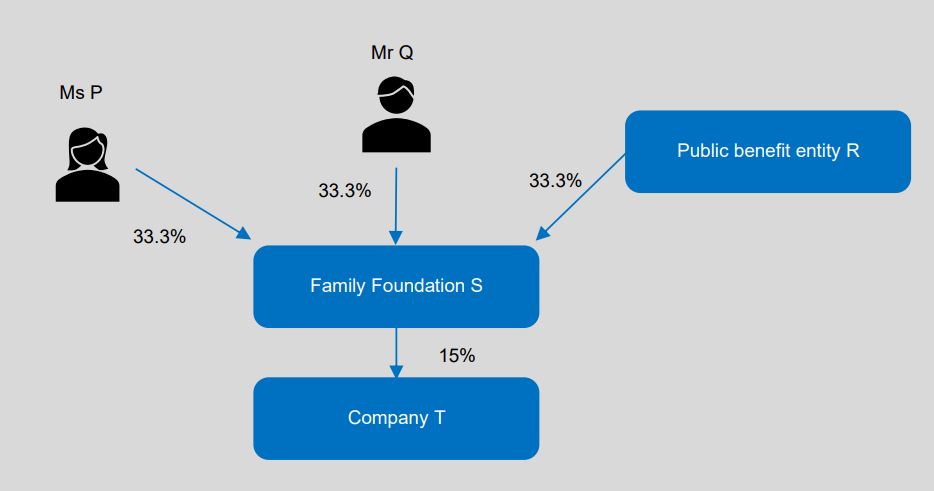

Distribution condition for Foundation SCorporate Tax treatment for Ms P and Mr Q