The Zakat, Tax and Customs Authority ('ZATCA', 'Authority') has issued this Guide for the purpose of clarifying certain tax treatments concerning the implementation of the statutory provisions in force as of the Guide's issue date. The content of this Guide shall not be considered as an amendment to any of the provisions of the Laws and Regulations applicable in the Kingdom.

Beta Version

Website Last updated:

July 3, 2026

Agents

VAT Guideline | Version One

July 2020

Contents

1. Introduction

1.1. Implementing a Value Added Tax (VAT) system in the Kingdom of Saudi Arabia (KSA)

1.2. Zakat, Tax and Customs Authority (ZATCA)

1.3. What is Value Added Tax?

1.4. This Guideline

2. Definitions of the main terms used

3. Economic Activity and Registration

3.1. Who carries out an Economic Activity?

3.2. Mandatory registration

3.3. Optional VAT registration

4. Agency

4.1. Concept of Agency for VAT purposes

4.1.1. Commercial Agencies Law

4.2. Principal or Agent?

4.3. Applying VAT to transactions made by Agent as Principal

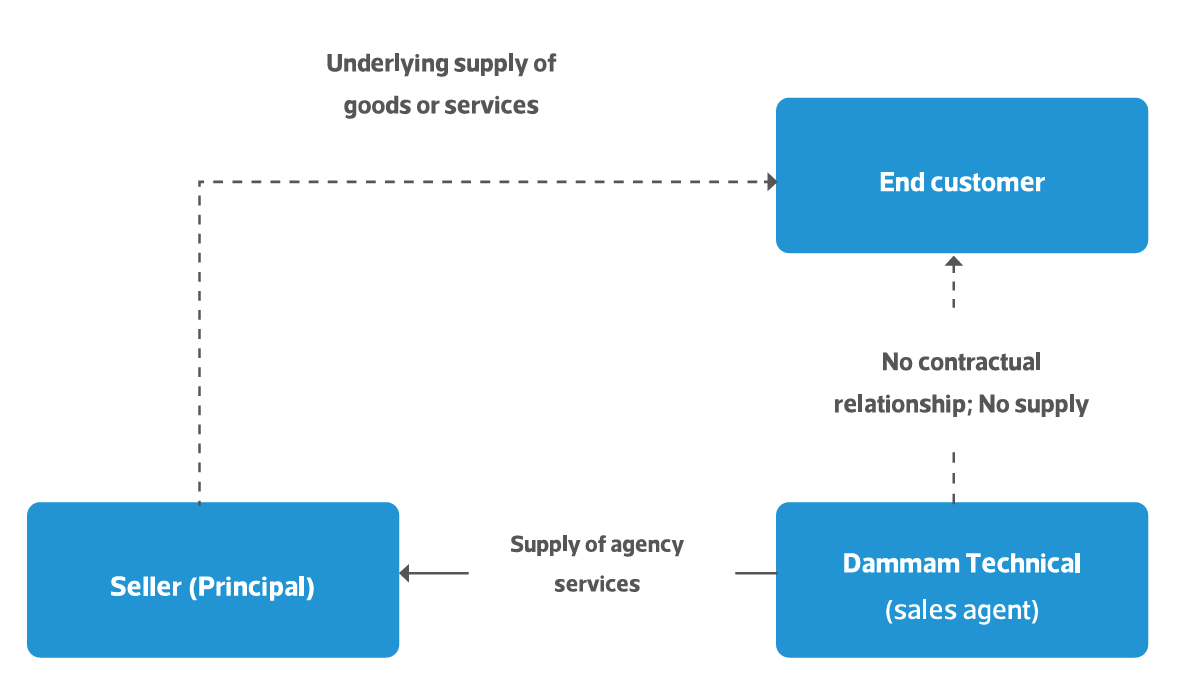

5. VAT treatment where Agent acts on behalf of Principal

5.1. Underlying supply made directly from Seller to End Customer

5.2. Supply of agency services made by Agent to Principal

5.3. Commission charged to non-KSA Principals

6. VAT treatment where Agent acts in his own name

6.1. When does an Agent act in his own name?

6.2. Agent is treated as a Principal for VAT purposes

6.3. VAT liability on supplies

7. Agent acting as Importer

7.1. Liability for import VAT

7.2. Deduction of import VAT

8. Charges of costs by Agents

8.1. Expenses incurred in name of Principal 'Disbursement'

8.2. Expenses incurred in Agent's own name 'Reimbursement'

9. Special cases

9.1. Travel agency

9.2. Land transportation services and ride sourcing applications

9.3. Financial intermediary

9.4. Hotel operators

9.4.1. Hotel operator acts as principal

9.4.2. Hotel operator acts as agent but in its own name

9.4.3. Hotel guest enters into a contract with the hotel owner

10. Input VAT Deduction

10.1. General Provisions

10.1.1. Input VAT incurred by Agents

10.2. Proportional deduction relating to input VAT

11. VAT obligations

11.1. Issuing tax invoices

11.1.1. Third party billing

11.2. Filing VAT Returns

11.3. Keeping records

11.4. Certificate of registration within the VAT system

11.5. Correcting past errors

12. Penalties

13. Applying for the issue of rulings (interpretative decisions)

14. Contact us

15. Frequently Asked Questions